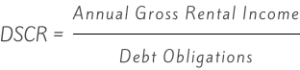

DSCR Formula Calculation

The debt service coverage ratio measures a property’s annual gross rental income against its annual mortgage debt, including principal, interest, taxes, insurance, and HOA (if applicable). Lenders use DSCR to analyze how much of a loan can be supported by the income coming from the property and to determine how much income coverage there will be at a specific loan amount. When calculating DSCR, lenders do not take into account expenses such as:

DSCR stands for Debt Service Coverage Ratio. This is a tool that helps a borrower’s ability to repay a loan by evaluating the property’s monthly rental income.

DSCR is a straightforward method of measuring cash flow, determined by dividing the monthly rent by the total monthly costs, which include the principal, interest, taxes, and insurance (together known as PITIA).

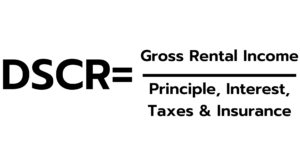

For commercial and mixed use property, DSCR is calculated by dividing the annual Net Operating Income (NOI) by the annual debt service (PITI). The difference with this approach is you are including the other operating expenses like utilities, maintenance, management fees, janitorial services, etc.

To calculate the DSCR, divide the subject property’s rental income by the monthly PITI (principal, interest, taxes, and insurance). Here is what the calculation looks like: Keep in mind that for commercial and mixed use properties they use Net Operating Income divided by PITI.

Keep in mind that for commercial and mixed use properties they use Net Operating Income divided by PITI.

Minimum Down Payment

DSCR loans, also known as investment property loans, Non-QM loans, or rental loans, have become very popular lately. But why all the buzz? While investors can still get traditional loans or funds from small banks, these options are difficult to qualify for and require significant cash reserves. DSCR loans are made for real estate investors and use the rental income from the property to help qualify for the loan. Let’s break it down.

Based on the Property’s Rental Income, Not Your Income

Experienced real estate investors or self-employed people without W-2s often have trouble meeting the strict requirements of conventional loans. These loans require good credit, high reserves, and proof of income. They are also underwritten using a Debt-to-Income (DTI) ratio, which compares your personal debt to your personal income. If you’re trying to get a loan for a rental property, the payment for that loan is included in your DTI calculation. You might be able to offset this new payment with rental income, but it depends on how well you can prove the expected rent. Investors with extra income from other sources might cover the gap in their DTI, but self-employed investors or those with multiple mortgaged properties might not have the extra income to make up for it. DSCR loans don’t use DTI at all. Instead, they look at the property’s rental income compared to the loan payments, making it easier for investors to qualify.

Borrow Through an LLC or Entity

Many investors prefer to borrow through an LLC or corporation to keep their personal information private and protect their other assets. This helps shield their personal assets in case something goes wrong with the property. Conventional loans can only be taken out in an individual’s name, but DSCR loans allow you to borrow through an LLC or other business entity.

DSCR Lenders Are More Flexible on Property Limits

With conventional loans, even if an investor can afford to take on several mortgages, they can only get loans for up to ten properties. Most DSCR lenders don’t have a set limit, instead looking at the total amount of credit the investor is exposed to and using common-sense guidelines.

Require Less Documentation

Conventional mortgage loans usually require a lot of paperwork, including pay stubs, bank statements, and tax returns. Underwriters thoroughly review your financial history, which can take time. Missing documents can cause delays. DSCR loans, however, focus more on the property’s value and rental income, as well as your credit. As a result, there is less paperwork needed. Most DSCR lenders won’t ask for proof of income, employment, or assets (except for liquid reserves).

While it is best to discuss your specific scenario with one of our Loan Agents, here are some general requirements:

Minimum Credit Score

We don’t have a minimum credit score, even though most DSCR lenders only go as low as 660 or 680. Most lenders also have a minimum tradeline requirement (amount and duration) reporting on your credit report, and also will consider if you have significant credit events, such as bankruptcies, foreclosures, and recent mortgage lates. Some lenders also require charge offs and collections be paid off prior to closing, although we do not require this.

If you don’t meet the credit requirements for a DSCR loan, you may be a better fit for our Hard Money loan option.

Minimum Down Payment or Equity

We can go as high as 80% LTV on purchase loans, and 75% LTV on refinance, depending on the property type, credit and DSCR ratio.

Minimum Property Value

We have a minimum property value of $100k. If you own multiple investment properties worth over $50k, ask us about our blanket loan option.

Minimum Loan Amount

Most lenders have a minimum loan amount of $100k. We can go as low as $75k.

When comparing DSCR loan lenders, it’s important to consider the following:

What are the lender’s rates and fees?

It’s essential to understand the full cost of the loan upfront. You don’t want to be caught by surprise with unexpected expenses at closing. Most lenders charge an origination fee, along with other administrative fees like underwriting and documentation fees. Additionally, be aware of any prepayment penalties, especially if you plan to sell the property soon after purchasing it. Most importantly, make sure you are dealing with a reputable lender.

Is the lender experienced in working with investors?

In our opinion, this is the most important factor to consider. Lenders who specialize in working with investors tend to have a better understanding of the unique needs and challenges of investment financing. As the market for DSCR loans grows, it’s helpful to look for lenders with experience. Here are some questions to ask potential lenders:

- How many DSCR loans have they closed?

- How long have they been offering DSCR loans?

- Do they have a dedicated team that processes and underwrites DSCR loans?

- What are their property insurance requirements (they may differ for investment properties versus owner-occupied properties)?

- Do they have prepayment penalties or rate buy-down options? Keep in mind that most DSCR loans include a prepayment penalty.

- Do they allow financing through an LLC or corporate entity?

Choosing a lender who has a solid track record and a specialized focus on real estate investors can make a big difference in the loan process.

We have options from no prepayment penalty to 5 years. The longer the prepayment penalty, generally, the lower the rate and cost will be. The pre-payment penalty may vary based on the loan, so it’s important to get those exact details from your loan agent.

A rate buydown in a mortgage allows a borrower to lower their interest rate by paying additional upfront costs, known as discount points, at closing. This can reduce monthly mortgage payments for a certain period or the entire loan term, depending on the type of buydown. Our suggestion is to speak with a Loan Agent directly about your scenario to see if a rate buydown makes sense, and which option makes the most sense, as it varies by each borrower’s individual situation.

Types of Rate Buydowns:

1. Permanent Buydown: The borrower pays discount points to secure a lower interest rate for the life of the loan. Typically, each discount point (1% of the loan amount) reduces the rate by around 0.25%, but this varies by lender. Example: On a $300,000 loan, paying $6,000 (2 points) might reduce the rate from 7% to 6.5%.

2. Temporary Buydown (e.g., 2-1 or 3-2-1 Buydown): The borrower (or sometimes the seller or lender) pays a lump sum to temporarily reduce the interest rate for the first few years. Common structures:

2-1 Buydown: Rate is 2% lower in year 1, 1% lower in year 2, and reverts to the original rate in year 3.

3-2-1 Buydown: Rate is 3% lower in year 1, 2% in year 2, 1% in year 3, then reverts.Often used by sellers to attract buyers or lenders to help affordability.

Pros and Cons of a Rate Buydown:

Pros: Lower initial mortgage paymentsCan make homeownership more affordable early onCan be beneficial if planning to refinance before the full rate applies (in temporary buydowns)Helps buyers qualify for a loan with a lower debt-to-income (DTI) ratio

Cons: Requires higher upfront cash If selling or refinancing early, upfront costs may not be recoupedCan be complex, especially temporary buydowns

While DSCR loans can be a helpful financing option for many real estate investors, there are certain scenarios in which using a DSCR loan may not be ideal. Here are some cases where a DSCR loan may not be the best choice:

- When purchasing a primary residence: DSCR loans are designed for investment properties rather than primary residences because the DSCR is calculated based on the rental income of the property. If you’re buying a home to live in yourself, you’d likely be better served by exploring traditional mortgage options tailored to owner-occupied properties.

- When you want to purchase distressed property/fix and flip a home: DSCR loans may not be suitable for purchasing distressed properties or for fix-and-flip projects where the intention is to quickly renovate and resell the property for a profit. In these cases, short-term financing options like hard money loans or bridge loans may be more appropriate due to their flexibility and faster funding times.

- When purchasing a property worth less than $100,000: DSCR loans are often more suitable for financing larger real estate investments with higher property values. For properties valued at less than $100,000, the transaction costs and underwriting requirements associated with DSCR loans may outweigh the benefits. In such cases, alternative financing options may be more practical.

Understand the interest rate on the loan, whether it’s fixed or adjustable, and how it will impact your monthly payments and overall cost of borrowing. Additionally, you should inquire about the duration of the loan, repayment schedule, and any prepayment penalties or balloon payments that may apply.

Ask about origination fees, discount points, closing costs, and any other fees associated with the loan to determine the total cost of borrowing.

Eligible property types can vary between lenders. Ask your lender about any restrictions on the types of properties that qualify for the loan, such as residential, commercial, rural, or multi-family properties.

Working with lenders experienced in DSCR loans is crucial because they understand the unique aspects of investment properties. Key features of experienced DSCR lenders include:

- Understanding investors’ needs to offer financing solutions that align with their investment strategies.

- Expertise in property analysis to determine their income potential and accurately calculate DSCRs, evaluate property cash flow projections, and determine loan eligibility based on property performance.

- A streamlined approval process because the lender understands the documentation requirements, underwriting criteria, and due diligence process for investment properties to facilitate efficient loan approval and funding.

- There should be multiple money sources that have an appetite for all types of DSCR Non-QM loans. The lender should not have one money source with one set of guidelines. Not all investment properties are equal; if the lender has access to funding from private equity, securitization, and large insurance companies, then your loan has a better chance of closing.

Good news! Your property is still eligible if it is vacant, as long as it is still in a livable condition. This applies to purchases, refis, and cash outs. Most lenders require the property to be tenant occupied for a refinance. We do not! Reach out to your Loan Agent to see if there will be any additional requirements or limitations based on your scenario.

How is the DSCR calculated on a vacant property?

We use a specific type of form ordered with our appraisal reports where the appraiser will also provide a report with a projection of the monthly rental income, based on comparable rental properties in your area.

Yes! We allow short term rental income for our DSCR loans. Reach out to your Loan Agent for more details.

To apply for a DSCR loan, the first step is finding a bank or lender with a robust DSCR loan program. JCREIG Capital Funding offers DSCR loans and has a history of qualifying borrowers at various income levels for small and large investment property loans.

Here’s an overview of how to apply for a DSCR loan with JCREIG Capital Funding:

- Fill out a loan application: Once you’ve chosen a reputable lender, it’s time to fill out a loan application. You can quickly apply for a DSCR loan through JCREIG Capital Funding using our online application, or you can call our office and have one of our Sr. Loan Officers fill out the application with you over the phone.

- Calculate your DSCR: Calculate the DSCR and fill out a rent schedule. The rent schedule validates the property’s fair market value, showing whether you can cover additional mortgage payments on a new property. Your DSCR will impact the interest rate that you qualify for.

- Lock in your interest rate: After calculating your DSCR and reviewing your application, we will offer you an interest rate for your loan. You can lock in this interest rate as we proceed through the final steps of the loan approval process.

- Get approved: Close the loan. You don’t need to bring proof of personal income or other information about your financial history. DSCR loan requirements are less stringent than traditional loans, making the closing go much faster.

- Loan is funded: Once the loan is approved, we will quickly fund it and deposit the loan amount into your escrow account.

Upon approval for our DSCR loan program, you’ll receive an estimate of the interest rate, closing costs, and monthly mortgage payments. Prepare to pay for an appraisal and undergo the underwriting process prior to signing the closing documents. The underwriting process includes credit report review, appraisal, rental income verification, title search, and a final underwriting decision.

{kind=link}