Leverage Your Portfolio And Expand Your Business With DSCR Rental Loans

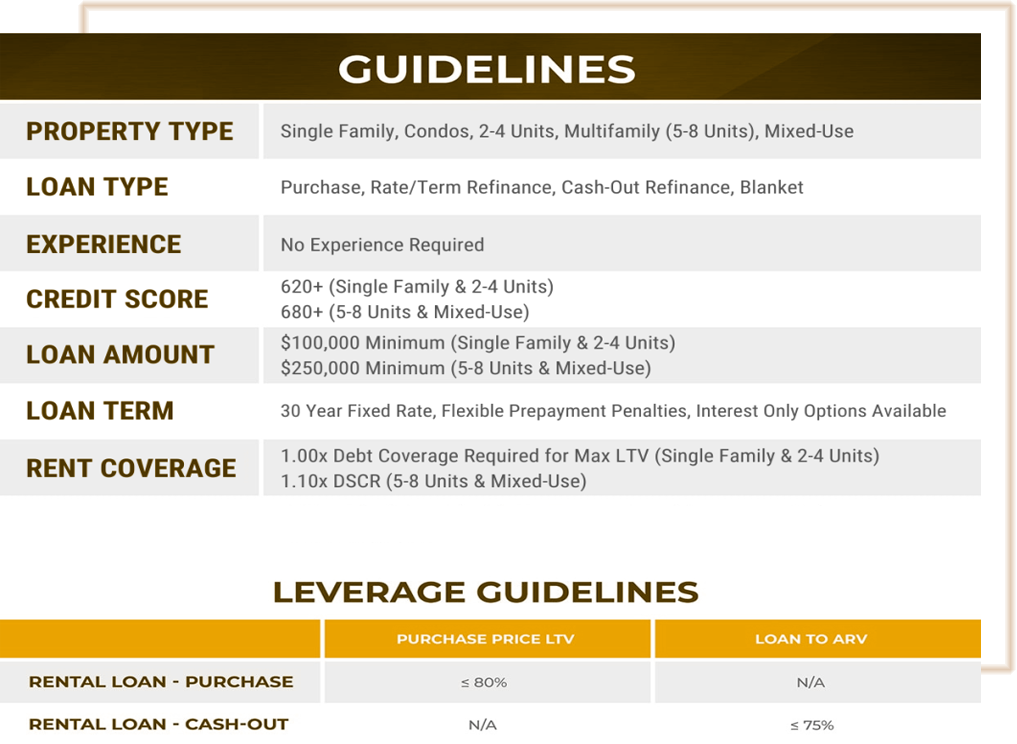

Up To 80% LTV

Purchase, Rate/Term, Cash Out

Long & Short Term Rentals

30Yr or 40Yr Fixed, 5Yr or 7Yr Arms, & Interest Only Available

LTV Stacking (Finance Your Fees!)

Foreign Nationals OK

Min DSCR: 1.00x

Qualify Based On Property Income

No Seasoning Required

New Investors Welcome

Start or expand your cash flow from your investment with a rental property loan, regardless of your experience. If you’re an investor and you’re looking for a way to increase your earnings through real estate, this program is a perfect fit for you.

At JCREIG Capital Funding, we provide real estate investors with tailored financing solutions designed to maximize their returns. Our DSCR (Debt Service Coverage Ratio) Loans allow investors to grow their rental portfolios quickly with 30-year or 40-year fixed, 5-year or 7-year arms. Also called “buy and hold” loans, this program requires little documentation and no prior real estate investing experience. Borrowers are qualified mainly on the property’s income/debt service coverage ratio (DSCR). This loan program can be used to purchase a property, refinance an existing property, or perform a cash-out refinance to access existing equity.

Many of our borrowers employ the “BRRRR (Buy, Rehab, Rent, Refinance, Repeat) Method” of real estate investing, using our bridge financing program in conjunction with our DSCR rental program. Our Bridge loans provide financing for the purchase and rehab and our DSCR program offers great 30-year or 40-year terms when refinancing a newly renovated property into a passive income-producing rental property.

Whether you’re purchasing, refinancing, or cashing out, our streamlined process, competitive rates, and expert guidance make it easier for you to grow your investments with confidence. Let JCREIG Capital Funding be your trusted partner in securing the financing you need to succeed.

What is a DSCR (Rental) LOANS?

Investment Properties Only

No Tax Return Needed

2-50 Property Portfolio Options

Keep in the name of an LLC

Close in 10-14 days (and even in as few as 7 days)

First Time Flippers Welcome

Higher Leverage with More Experience

We Pay Brokers

Frequently Asked Questions

Debt Service Coverage Ratio. This is simply = your total payment / your total rents. If this number is 1.0 or greater, than your rents are higher than your total payment. The higher that is, the better your rate generally is.

The ratio is calculated by dividing the property income (rental income) from the property PITIA (principal + interest + taxes + property insurance+ homeowners association dues). The resulting ratio lets the lender know how much income is available to pay the mortgage. A ratio of 1.0x means that the property that the revenue from rental income AND expenses is equal. A DSCR above 1 means the property is positively cash-flowing. Conversely, a DSCR of less than one means that the expenses exceed the rental revenue and the property has a negative cash-flow.

Our DSCR loans are tailored to consolidate and restructure existing debts, providing more favorable terms and extended durations. This can lead to reduced monthly payments and more efficient debt management, ultimately bolstering your long-term financial health.

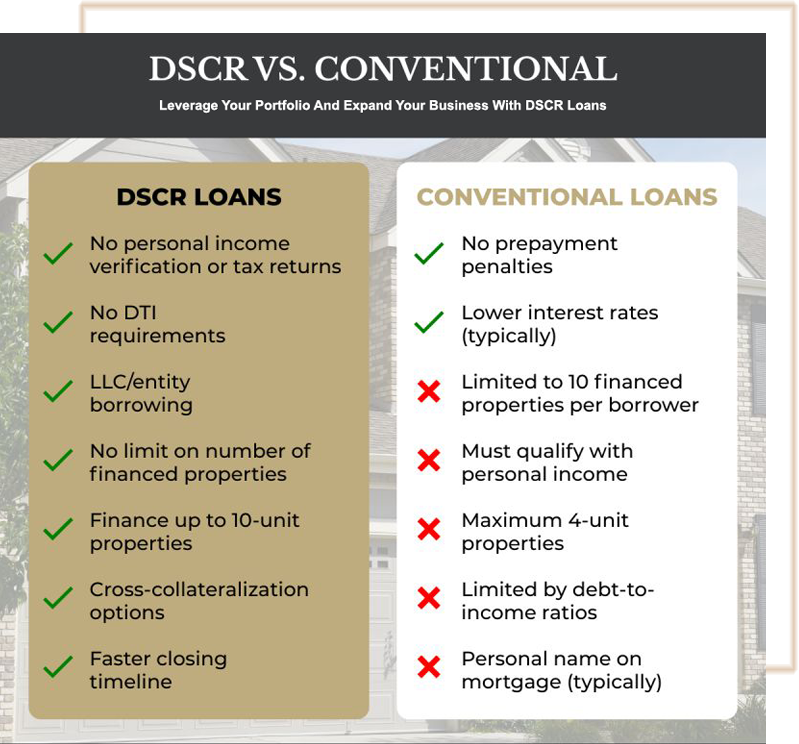

There’s many reasons clients prefer DSCR loans vs. Conventional financing. First, DSCR loans do not take into account your other debts beyond the PITI payment of your loan. So, if you are self employed and report very little income, using a DSCR loan may be the best option.

Secondly, a DSCR loan does not report to credit, and therefore may not affect your future ability to qualify for additional properties.

Another benefit is that a DSCR loan allows you to vest in an LLC , whereas FNMA does not allow that on traditional financing.

- No Personal Income or Employment Verification required.

- Faster closing process

- Very competitive rates

- Allows a real estate investor to change a Short Term Loan such as a Fix and Flip, Bridge and Ground up Construction to a 30 year Loan.

The top 3 factors that affect the DSCR rate include the actual Debt Service Coverage Ratio (DSCR), Loan-to-Value, and your FICO (credit score). The higher the DSCR is on a property, the lender is able to forecast a lower risk for lending the capital since the property may be positively cash-flowing and the investor is able to pay the monthly loan payments. Loan-to-Value, or LTV, refers to the loan amount as it relates to the actual value of the property. Typically, DSCR loans will never exceed 80% LTV. That means that the borrower needs to bring about 20% +closing costs as a down payment for the loan. The lower the LTV, the less risk for the lender, hence a better rate. Finally, your credit score is still a factor when determining the rate. Lenders use the score and it affects the final rate for your DSCR loan.

DSCR loans are different from traditional mortgage loans in several key ways, making them particularly well-suited for real estate investors. Here are the main distinctions:

Income Verification

Unlike conventional loans, which often require detailed personal income documentation such as W-2s, pay stubs, or tax returns, DSCR loans focus solely on the property’s income. This means your personal income doesn’t play a significant role in loan qualification, making DSCR loans an attractive option for investors who may not have traditional employment income or who prefer to keep their finances separate from their investment properties.

Qualification Criteria

For conventional loans, lenders generally use the borrower’s debt-to-income (DTI) ratio to determine eligibility. The DTI ratio compares your personal monthly debt payments to your income, and many conventional loans require a DTI ratio of around 43% or less.

In contrast, DSCR loans are based on the property’s cash flow, as measured by its DSCR. If the rental property generates enough income to cover the debt payments, the borrower is more likely to qualify for the loan. This allows investors to secure financing based on the strength of their investment properties, even if their personal finances don’t meet conventional loan criteria.

Loan Purpose

DSCR loans are designed specifically for investment properties, whereas conventional loans can be used for personal residences or second homes. Investors who need to finance rental properties, whether for long-term or short-term rental, will find DSCR loans more advantageous because they are structured around the property’s income-generating potential.

Loan Limits

Conventional loans typically come with strict loan limits set by entities like Fannie Mae and Freddie Mac. DSCR loans, on the other hand, are often more flexible, allowing for higher loan amounts since they are designed for real estate investors who are dealing with larger, income-producing properties.

Rates vary daily, but typically DSCR loans are .5% to 1.5% higher than a Conventional Loan. However, DSCR loans are much easier to qualify for given the fact they do not take into account your personal income.

Real estate investors increasingly turn to DSCR loans as a financing tool for their rental properties, and for good reasons. Here’s why DSCR loans are a top choice among savvy investors:

Simplified Qualification

With DSCR loans, you don’t need to go through the hassle of providing extensive personal income documentation. As long as your property generates sufficient cash flow to cover the loan payments, you’re in a strong position to qualify. This can make the loan approval process faster and less cumbersome, especially for investors with complex income structures.

Scalability for Portfolio Growth

Investors looking to scale their portfolios need financing that adapts to their goals. DSCR loans make it easier to qualify for multiple properties, as they focus on the financial performance of each individual property rather than your overall financial situation. This allows for faster acquisition and easier refinancing, helping you grow your portfolio more efficiently.

Leverage the Property’s Cash Flow

A DSCR loan allows investors to leverage the income potential of their properties. By securing financing based on the strength of the property’s income, rather than your personal financials, you can access funds to acquire more properties, renovate existing ones, or refinance for better terms—all while focusing on the financial performance of your investments.

Flexibility in Financing Terms

DSCR loans often come with customizable terms, such as interest-only payments, longer loan durations, and flexible down payment requirements, allowing investors to structure financing in a way that best supports their investment strategy.

Before diving into a DSCR loan, it’s important to understand the different elements that play a role in the approval process and the loan’s overall structure. These elements can vary by lender, but here are the most common factors you need to know:

Debt Service Coverage Ratio (DSCR)

As we’ve discussed, the DSCR is the cornerstone of these loans. Lenders will calculate the ratio to determine if the property generates enough income to cover the debt payments. While each lender has its own requirements, most will look for a DSCR of 1.0 or higher, though some may require a DSCR of 1.25 or more for additional security.

Loan-to-Value (LTV) Ratio

The Loan-to-Value (LTV) ratio measures the loan amount relative to the property’s value. Most lenders will offer DSCR loans with an LTV ratio of 75% to 80%, meaning you may need to make a down payment of 20% to 25% of the property’s purchase price. A lower LTV means less risk for the lender, while a higher LTV can make it easier to acquire properties with less upfront capital.

Interest Rates

Interest rates on DSCR loans can vary based on several factors, including the property’s location, your credit score, and the DSCR itself. Generally, DSCR loans may have slightly higher interest rates than conventional loans due to the focus on investment properties, which carry higher risk. However, the trade-off is the flexibility and ease of qualifying, making it worth the cost for many investors.

Prepayment Penalties

Some DSCR loans may include prepayment penalties, meaning you’ll be charged a fee if you pay off the loan early. This is something to watch for, especially if you plan to sell or refinance the property in the near future. Be sure to discuss these terms with your lender and factor them into your overall investment strategy.

Loan Terms

DSCR loans can be structured with a variety of term lengths, typically ranging from 5 to 40 years. Longer terms can help lower your monthly payments, while shorter terms can allow you to pay off the loan faster. Additionally, some lenders may offer interest-only payments for a period of time, which can reduce initial costs as you stabilize your investment.

Not all lenders are created equal, especially when it comes to specialized loans like DSCR financing. As a real estate investor, finding the right lender can be the difference between a smooth process and a frustrating one. Here’s what you should consider when choosing a DSCR lender:

Experience with Investment Properties

Look for lenders who specialize in working with real estate investors and are familiar with the nuances of investment property financing. JCREIG Capital Funding, for example, focuses on providing financing solutions specifically for real estate investors, giving us the expertise to understand your unique needs and challenges.

Flexible Loan Terms

Every investment is different, so you need a lender that offers flexible loan terms to match your strategy. Whether you’re looking for interest-only options, customizable loan durations, LTV stacking, or adjustable down payments, choose a lender that provides flexibility in structuring your loan.

Reputation and Customer Service

It’s important to work with a lender that has a strong reputation for customer service and reliability. Read reviews, talk to other investors, and ask questions to gauge the lender’s responsiveness, support, and overall professionalism. A trustworthy lender will work with you throughout the loan process to ensure that everything runs smoothly and that you’re getting the best possible terms for your investment.

Speed of Loan Approval

Real estate investing often moves quickly, so it’s essential to partner with a lender that can offer fast approval and funding times. Some lenders, like JCREIG Capital Funding, specialize in streamlined approval processes, enabling investors to move forward on opportunities without unnecessary delays.

In conclusion, DSCR loans are a powerful financing tool for real estate investors looking to scale their portfolios and maximize cash flow. With a streamlined approval process that focuses on the property’s income rather than personal finances, these loans provide flexibility, speed, and scalability for investors of all experience levels. When selecting a lender for your DSCR loan, prioritize experience, transparency, and customer service to ensure you get the best financing solution for your needs. JCREIG Capital Funding offers all of these qualities, making us a trusted partner in helping real estate investors achieve their goals.